Financial Planning – Step 3 – Determine Your Net Income

1. Background

The next step is to determine your net monthly income.

Most Financial Planning steps at this stage might involve setting up your financial goals. Typically this means setting up your

- Short-term goals which range from 1 month to 12 months

- Mid-term goals which range anywhere from 2 years to 5 years

- Long-term goals which range from more than five years and beyond

Do not get me wrong we are still going to tackle setting your Financial Goals, but for now, let us follow the outline used in the Wealth Dashboard that I recommended you buy from mywealthdiary. For now, let us figure out our net income which we shall use when coming up with our monthly budgets and annual spending plan.

Read: Financial Planning – Step 2 – Determine Budget Categories and Sub-Categories

For purpose of creating this financial plan, our main focus is going to be Net Income rather than Gross Income.

2. Net Income vs Gross Income

Your net income is what you bring home after all deductions have been made such as taxes and insurance. This is the amount that is deposited into your bank account.

On the other hand, gross income includes all additional earnings that you can possibly receive for doing your job or a project. Additional things that come as benefits from your job can include transport or housing allowances. These items might be included as part of your gross income so it is important to know which items are taxable and which items are not.

At the end of the day, knowing, whether to use gross income or net income when creating your budget, is crucial. My personal preference is to concentrate on your net income when making a budget. This is simply because this is money you can control. Money that actually hits your bank account.

3. Determine your Net Monthly Income

Your income does not necessarily only come from the money that you receive from working at the job. Therefore we are going to categorize incoming into two main categories.

- Main income

- This category will include well-known regular income other than your salary and wages. Examples of other sources of main income include:

- Interest

- Dividends

- Bond Coupons

- Royalties

- Child Support

- Social Security & Pensions

- This category will include well-known regular income other than your salary and wages. Examples of other sources of main income include:

- Side hustles

- This category will include net income received from any extra activities. Examples of side hustle income include:

- Commissions

- Small Business Income / Profit

- Tips

- This category will include net income received from any extra activities. Examples of side hustle income include:

Depending on where you are in your financial journey your net income might only be 2 or 3 sources. That is fine because you can add more income sources as you go.

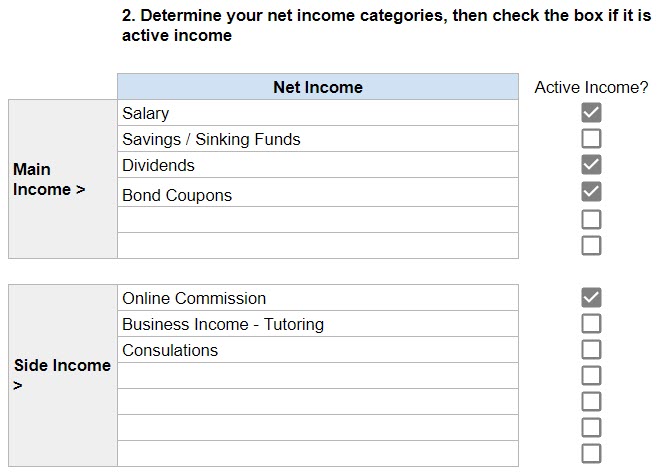

4. Enter Income Categories in Wealth Dashboard

The great thing about the Wealth Dashboard is that once you enter your information once it will propagate to all the necessary worksheets which creates great charts and visuals.

After you have entered your income sources, your dashboard should look like the image on the right. In the long run, the dashboard will be able to give you statistics and charts based on which income source is the highest and lowest. For now, your income source might only be one which is your main job. But over time as you start to invest and save your money your income categories will also grow.

One last thing

What do you do if your income is not consistent?

If your income is hard to predict because of the nature of your job. Then tracking your expenses and budgeting are a must for you. The last thing you want is a situation where the money comes in and equally moves out of your life with notice or purpose. That means yet again, you need to be aware of your spending by tracking it. Here are some simple things you can do when you have inconsistent income.

- Action Step 1

- Therefore, the best way to budget if you have inconsistent income is to base your income on your lowest-paid month from the previous year. It’s better to be under budget than to over budget your income.

- Action Step 2

- Moving forward you will have to prioritize your expenses. Using the Budget Categories set in Step 2, you reorganise and highlight expenses that are the most crucial (items like food, clothing, shelter, and transportation, as well as making the bare minimum debt payments) to things you can go without such as DStv, eating out and fun money.

- Action Step 3

- Another goal to work towards over time is to try and ensure your net income is one month ahead. This goal can take some time so do not try and do it all in one goal. Using the important expense you decided in step 2 above. You will be able to Know how much you need in your buffer.

5. Actionable Tasks

These steps’ actionable tasks are simple enough but require some thought and also re-doing depending on what income sources you expect to have throughout the year. For now, it might just be your salary or wages but over time as you start to invest and increase your income sources. The income categories will also change.

The following are the tasks that you need to complete. After you finish a task, you can tick it off just to help you keep track of what you have done and what else is pending.

Your Wealth Dashboard should be coming together now. Only 3 more sections are left and then we tackle the biggest step in Financial planning which is setting your Financial Goals. Actually, we are going to leave Section 6 which is Determine your Debt Categories and then come back once we are done with the financial goals.

You are doing amazing so far 👏👏👏